Dec 13, 2024

This is an archive of our post on Aave governance forum. Read the full thread here.

Summary

LlamaRisk supports the proposed parameter changes to increase capital efficiency. While the more permissive Liquidation Threshold (LT), Loan-to-Value (LTV), and Liquidation Bonus (LB) parameters increase the likelihood of bad debt during high volatility periods through increased liquidation risk and decreased liquidator profitability, these risks are assessed as low. @ChaosLabs analysis shows users typically maintain healthy risk factors when borrowing non-correlated assets against similar collateral, as demonstrated by user behavior with assets like wstETH. Additionally, weETH’s high liquidity and historical stability near its peg further mitigate the risk of bad debt.

Purpose

@ChaosLabs proposes increasing LTV by 5% to 77.5%, LT by 5% to 80%, and decreasing the liquidation bonus (LB) by 0.5% to 7%. This is done on Aave’s ETH Core instance. This aims to increase weETH’s capital efficiency, which enables those supplying weETH to increase the amount they may borrow against it. The change is expected to increase TVL, borrow potential in general, and borrow interest paid, adding utility for users and the protocol.

Expected outcome

This change brings the asset almost the same parameters as wstETH (LTV 78.5%, LT 81%, LB 6%). The small difference between these two parameter accounts for increased risk using weETH as a collateral asset (more in the next section).

weETH is currently included in the “ETH Correlated” liquid E-mode, meaning that this is not the highest LTV / LT and lowest LB users can achieve on Core. This asset is not onboarded to Prime.

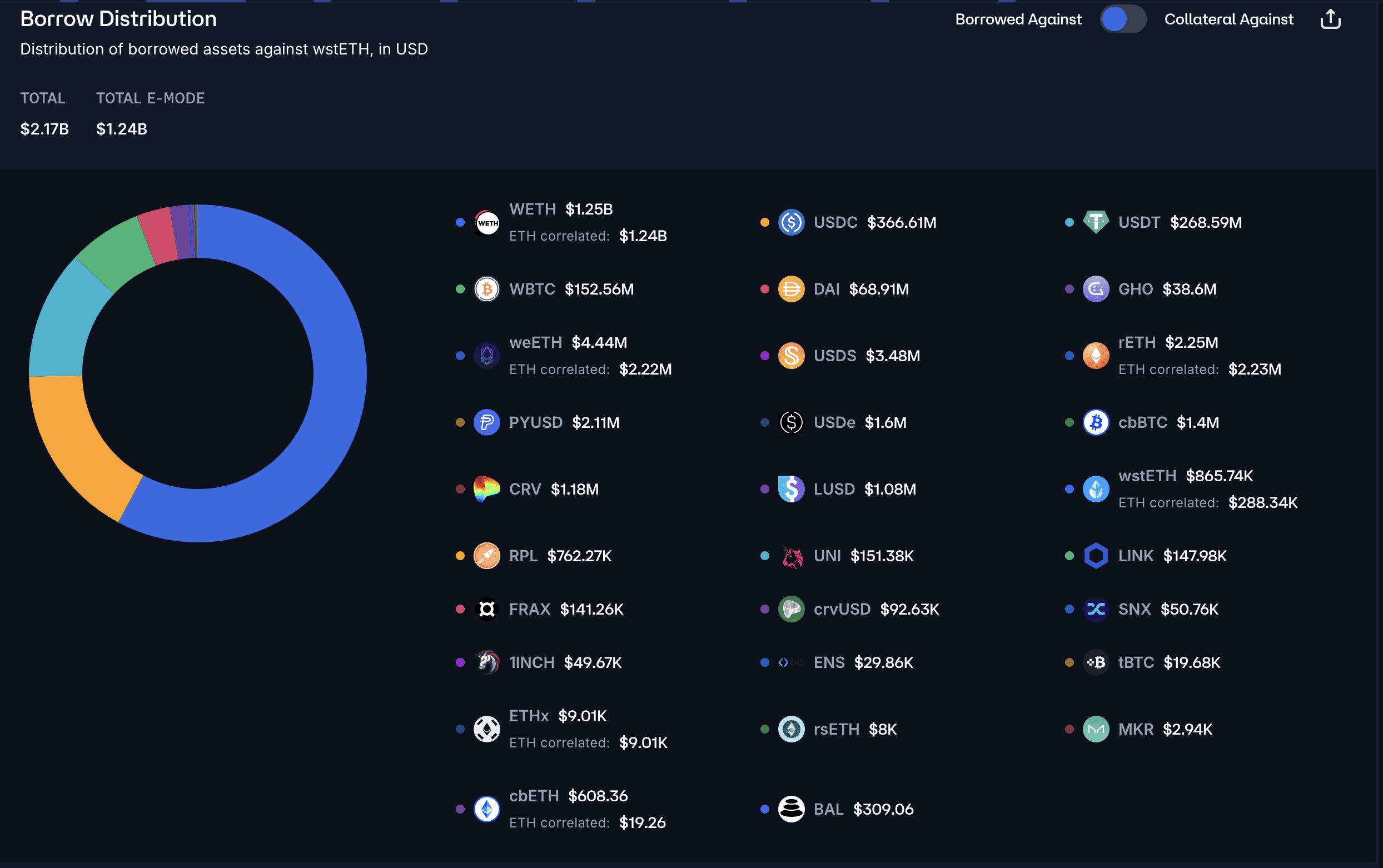

Source: Chaos Labs Community Dashboards, wstETH, 13th December 2024

@ChaosLabs comment above notes that 96% of weETH borrowing is done inside the ETH Correlated E-mode. This parameter change will make weETH a more attractive asset to borrow non-correlated assets for leveraged trading or delta-neutral farm other assets onchain.

@ChaosLabs borrow distribution visualization demonstrates many users still borrow WETH in the ETH-correlated E-mode. However, ~$700M in non-correlated assets (chiefly USDC, USDT, and WBTC) are also being borrowed. With these parameter changes, weETH collateral usage may reflect this pattern, with substantially more non-correlated debt being taken on.

It is important to note that decreasing the liquidation buffer may reduce the potential profit a liquidator may receive should they liquidate debt positions that weETH inadequately collateralizes.

Potential risks

The primary risk of this change is potential bad debt to the protocol stemming from two factors:

Increased likelihood of users reaching liquidation thresholds by borrowing uncorrelated debt during times of volatility, in extreme cases potentially causing liquidation cascades (possibly exacerbating bad debt generation)

Decreased liquidation bonuses resulting in increased hesitancy from liquidators to purchase undercollateralized positions.

The second risk is especially worth considering given weETH is restaked ETH, meaning its price may deviate from underlying ETH collateral.

A secondary risk is that users may consider this asset analogous to wstETH in the risk profile. weETH is a higher-risk asset in various ways: architectural, economic, governance, access control, and dependency. Users may see the parameters are broadly similar and presume the risk profile is the same. This is not the case, and they may be liquidated without fully understanding why. For more on these risks, see our report on weETH from Q1 of this year.

Likelihood of risks

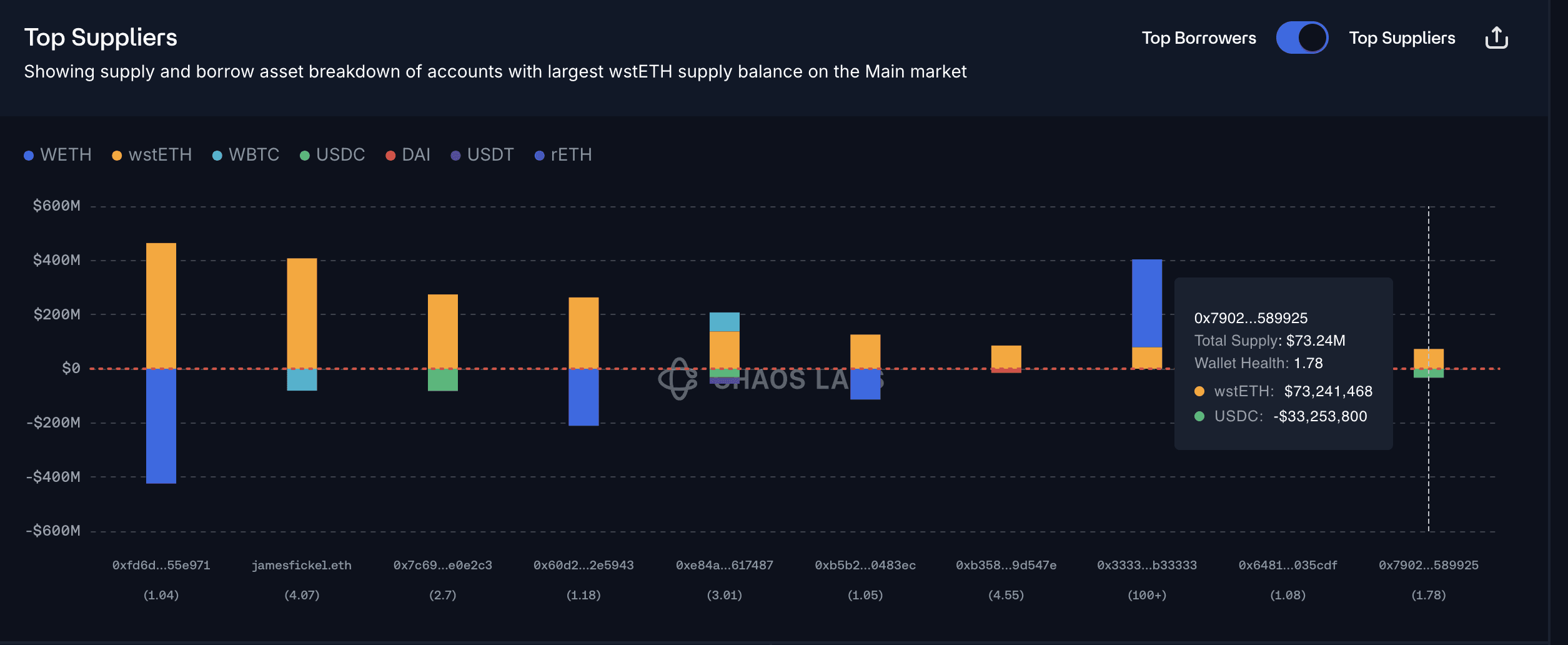

Source: Chaos Labs Community Dashboards, wstETH, 13th December 2024

Liquidators may struggle to liquidate large depositor positions during volatility due to reduced onchain liquidity. We can see that “whale” health scores on wstETH are high (with the lowest at 1.78). Only significant drawdowns will likely bring these users into the liquidation threshold range. wstETH would have to decrease in price by >33% in an extremely short period for the most aggressive large non-correlated borrow address (at 1.78 health score) to reach that liquidation threshold. While flash crashes are increasingly possible from overleveraging (as we saw recently with BTC), an intraday price decrease of such size has occurred very few times. Daily average price volatility in the past 12 months is 5%. This makes the first risk low likelihood.

The second risk is also unlikely, given weETH’s limited price deviation from the peg. As @ChaosLabs notes above, onchain liquidity is sufficient to handle a >$30M weETH swap to stablecoins at a 4% price impact, and weETH exchange ratios to underlying collateral do not deviate significantly (in recent history).

Disclaimer

This review was independently prepared by LlamaRisk, a community-led non-profit decentralized organization funded in part by the Aave DAO. LlamaRisk is not directly affiliated with the protocol(s) reviewed in this assessment and did not receive any compensation from the protocol(s) or their affiliated entities for this work.

The information provided should not be construed as legal, financial, tax, or professional advice.